Trend Following is a lifestyle. It is a way of thinking, acting and doing. It does take determination, however. It isn’t easy to make money from the markets, just as it isn’t easy to become an Olympic athlete. Think of all the factors about yourself that would need to be altered if you were to train for the Olympics. Your diet, fitness routine, coaches, psychology and so much more would have to be worked on tirelessly to make it to the top. Your whole lifestyle and way of being would need shift. You would have to put the time in.

Now lets put that into trend following terms. You cant expect to read only a book (even though mine are a great first step), with no work on your end, and magically make millions in the markets. If it were that easy everyone would be making the big money. It takes practice, patience and perseverance. You can memorize algorithms or imagine the “perfect” system all you want, but until you master your psyche you will never reach your full potential. This is why Charles Faulkner (listen) has been on my podcast three times and is easily one of the most popular guests.

You should be skeptical of anyone who claims to be able to predict the future from the past. If it were so easy to beat the market using past returns, everyone would exploit that relationship until it is arbitraged away. The momentum effect violates that principle. Momentum is based on the premise that securities that have recently outperformed will continue to do so in the short run, and those that have underperformed will continue to lag. While practitioners have been exploiting this relationship for decades, the idea has gained broad acceptance in the academic community only within the past 20 years. Momentum runs counter to the predictions of the efficient market hypothesis, but the evidence is too overwhelming to ignore.

Jegadeesh and Titman published one of the first influential studies on momentum in 1993, “Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency.” They found that U.S. stocks with the best performance over the past three-12 months continued to outperform the worst-performing stocks over the next year, using data from 1965 to 1989. Subsequent research found that the momentum effect was also present in the U.S. before and after this original sample, which suggests that the effect was not simply the product of data mining. Generally any momentum signal between six and 12 months worked, though there tends to be a short-term reversal at one month. It has become convention among many researchers to study the momentum effect using stock returns over a trailing 12-month period, excluding the most recent month. However, the results are robust and do not depend on this particular definition.

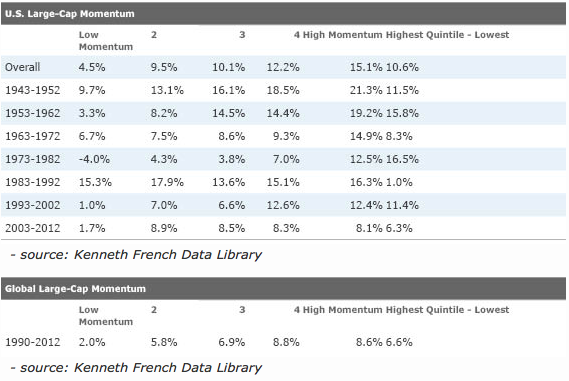

Momentum is pervasive. Many studies have extended this evidence to foreign stocks, commodities, currencies, and bonds. Momentum even works across individual asset classes and country stock indexes. Even efficient market advocates Eugene Fama and Kenneth French found the momentum effect in every stock market they studied, except Japan (see “Size, Value, and Momentum in International Stock Returns”). The tables below illustrate the momentum effect among large-cap U.S. and global stocks. Each column represents a fifth of the total number of stocks in the sample, which are ranked by their momentum. While there is not a linear relationship between the momentum quintiles, stocks with the highest momentum consistently outperform those in the lowest momentum quintile. Small-cap stocks tend to exhibit a stronger momentum effect. However, they can be more expensive to trade.

This evidence creates a puzzle. If the market were efficient, a simple trading rule should not produce superior returns. Arbitrage is a powerful force that should eliminate any excess profits, and yet, momentum has persisted 20 years after it was first widely published. Perhaps more troubling to disciples of Ben Graham and Warren Buffett, momentum appears to be at odds with decades of research, which suggest that stocks trading at low valuations tend to outperform.

Explanations

Behavioral finance offers the best explanation for the momentum effect. Those in this camp assert that investors tend to anchor their beliefs and are slow to update their views in response to new information. For instance, event studies have demonstrated that stocks that beat earnings expectations tend to offer excess returns for many weeks after the announcement. Similarly, stocks that miss expectations tend to continue to underperform. Behavioral finance research also suggests that many investors engage in irrational mental accounting, which may further contribute to this market underreaction. According to this view, investors are reluctant to sell losers in the hope of breaking even and quick to sell winners in order to lock in gains. This irrational behavior may prevent stocks from quickly adjusting to new information. Once a trend is established, investors may pile onto a trade and over extrapolate recent results, pushing prices away from their fair values, which may explain the long-term reversals underlying the value effect (the tendency for stocks trading at low valuations to outperform).

Momentum is consistent with the value premium and may even contribute to it. While momentum tends to persist in the short term (performance over the past six-12 months continues over the next few months), stocks that have been beaten down over the past three to five years tend to do better than their counterparts that outperformed over that horizon. Where this value effect allows investors to profit from the market’s pessimism, momentum allows investors to profit from its optimism. In their paper, “Value and Momentum Everywhere,” Asness, Moskowitz, and Pedersen found that momentum worked well when value didn’t, and vice versa. Because they are two sides of the same coin, each with excess returns, combining value and momentum in a portfolio can offer powerful diversification benefits.

Risks

Although momentum looks good on paper, these strategies require high turnover, often in excess of 100%, in order to work. That can create high transaction costs that may erode profits. Additionally, momentum does not work well when volatility spikes. Consequently, the strategy can underperform when it is most painful. For instance, momentum significantly underperformed during the 2008 global financial crisis. Unlike value strategies where lower valuations predict better long-run returns, it is difficult to gauge when momentum is likely to outperform. This risk may limit arbitrage and allow momentum to persist. In fact, there are only a handful of pure momentum funds available to most investors.

Recommendations

While a diversified and systematic momentum strategy can offer a powerful way to enhance returns, selecting a few stocks on the 52-week high list is a very bad idea. It is difficult to anticipate when a run will end and there may be no greater fool to bail you out. Although momentum is a short-term phenomenon, it is best suited for long-term investors. It won’t always work, but there’s a good chance that a disciplined momentum strategy will continue to outperform over the long term. After all, investor behavior won’t change overnight.

AQR Momentum (AMOMX), AQR Small Cap Momentum (ASMOX), and AQR International Momentum (AIMOX) offer investors an effective way to harness momentum. Each of these funds invests in stocks representing the third of their respective market segments with the highest momentum. AQR balances transaction costs against momentum when deciding whether to trade, which helps rein in expenses. However, because these funds have high turnover, they are most suitable for tax sheltered (retirement) accounts. While the $5 million minimum investment may seem a little steep, there is no minimum for investors who gain access to these funds through a financial advisor.

PowerShares DWA Technical Leaders (PDP) may be a suitable alternative for investors who do not have a financial advisor. This fund targets 100 stocks with the best performance from a broad universe of U.S. large- and mid-cap stocks, and weights them according to their relative strength (a form of momentum). In order to reduce turnover, PDP rebalances only quarterly, which can hurt its performance when the market is choppy.

Combining Value and Momentum

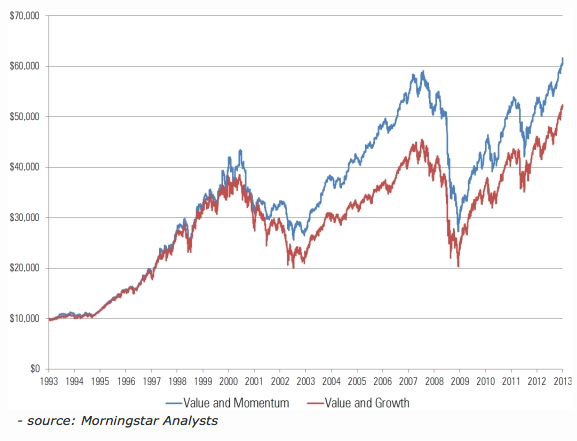

It’s not necessary, or advisable, to abandon value investing to benefit from momentum. Instead, momentum may be a good substitute for investors’ growth allocations. Momentum offers higher expected returns than growth and tends to be less correlated with value. The chart below compares the performance of a portfolio consisting equal weights in the Russell 1000 Value and Growth indexes, with a portfolio that replaces the growth allocation with the AQR Momentum Index. The two portfolios have similar volatility, but the value and momentum portfolio offers slightly better absolute and risk-adjusted returns.

My guest today is Jerry Parker. In 1983, Parker was accepted into the Turtle Program, a select investment training program developed by successful Chicago portfolio manager Richard Dennis. He appears in Covel’s “The Complete TurtleTrader” and has been the most successful TurtleTrader. Parker founded Chesapeake Capital Corporation, a global investment manager headquartered in Richmond, Virginia, in 1988.

The topic is Trend Following.

In this episode of Trend Following Radio we discuss:

Mistake of combining different strategies with trend following, and the importance of having a concentrated strategy that you can rely on

How discretionary moves can get in the way of your system, and “systematized discretion”

The psychological effect of following a trend following strategy for decades

The idea of going for positive expected value over what’s least risky

Why Parker doesn’t like to use the term “managed futures”, and why it doesn’t really tell the story of trend followers

Trend followers performing well at different points in time compared to long-only

Using trend following as another strategy for investors who only invest through a long-only value-based system

The importance of not letting your views on politics and society influence your trading, and maintaining a systematic and disciplined approach

The growth of news media since 1984, information overflow, limiting your variables, and using price as your primary indicator

How Parker has learned over the years to deal with drawdowns, loving your losses, and the importance the Turtle program played in his education on drawdowns

Why governments are the ultimate counter-trend traders

Why buy and hold is not a good place to be even if people are saying it’s turned around

Parker’s stock-only trend following program, and why the diversified program will do better than the stock-only system

Leverage as a tool

Listen to this episode:

Listen to this podcast on iTunes. (Please leave a rating!)

Hi Mike, Just listened to your last podcast. Thanks for doing the podcasts while you are on the road! Trading is a solitary activity, I have not found any other trend following traders locally. I find people just want to discuss fundamentals and sentiment and predictions. No good for the business of non-discretionary trading. So I find listening to your interviews balances that, almost like having access to mentors. I’m always looking forward to the next interview. The monologue episodes are sometimes puzzling however, particularly your negative comments aimed at various groups. This time it was daytraders. I am not a daytrader and don’t want to be, its not my style, but I do know people who earn good profits daytrading. But why should you or I care if they have their eyes glued to the screen, its their own choice and it doesn’t effect us. I’m assuming your long term aim is marketing your stuff (an honorable objective, all credit to you for that), but is talking down to potential customers really effective? Also something confused me with your logic today, you make the assumption that any historic data correlated with trend following, must therefore also be derived from trend following. But could daytrading profits also be correlated? eg. Oct 2008 trend following was profitable, but surely daytraders would also be short as markets were consistently directional downwards, so they would also be profitable from the high volatility. My logic might be wrong, let me know. By the way I’m a big fan of your books, and recommend them at every opportunity. Most of my foundation concepts came from reading “Trend Following” about 3 years ago, but I also liked “Trend Commandments” for clarifying the whole TF mentality.

Regards,

Mike B.

In my books are performance track records of trend following traders. Audits. Where are the day trading records like that? My passion is to take what I know and pass it along. Clearly, I am not the only one who shares that day trading view. You are aware of Ed Seykota? Why would potential customers be offended by my comments? Confused. Also, clarify your point about correlations? Not following that logic.

Hi Mike, Thanks for your reply. Why could they be offended? “They have personal issues they try to resolve by daytrading…” Did you mean that in a complimentary way? But I don’t disagree with your Ed Seykota quote about daytraders. My point about marketing is that getting a negative gut reaction from potential customers doesn’t usually result in them reaching for their wallets. Its not offensive to me, I’m not in that group. Personally I prefer to only make decisions once a day, and play more golf! This is how I see the relationship between trend following and daytrading. I view all market activity (all time frames) as driven by two character types, either momentum/TF or reversion-to-mean (RTM). The RTM guys include value investors, most analysts, and most media commentators. Any healthy market needs both TFs and RTMs, but each individual person can’t be both. In sideways markets you can’t tell the difference, but when prices are moving into new territory thats when the two types polarize. When price is making new highs/lows TFs want to be in the trend direction, and RTMs want to be opposite, and the trend stops only when RTMs overwhelm the TFs. But those same two drivers come into play when medium-term traders look at a daily chart, or when daytraders look at a 5-min chart. A daytrader can have a TF style (buying new highs, etc). The difference is the speed, the intensity, and higher probability of being knocked out by market noise. Anyway, you’ve been doing this much longer than me, I could be wrong. So thanks for letting me voice an opinion. Enjoy the rest of the weekend!

Cheers,

Mike

Calgary, Alberta

Thanks Mike for the thoughtful note, but let me be even more stark:

1. Day trading track records don’t appear to exist.

2. If a strategy is faulty, or doesn’t work, or there is no proof, why would you keep hoping for it to work or imagining it to work? Yes, that would lead to Ed Seykota’s conclusion about “issues” that they need to work on.

Michael, Hope you are enjoying your journey. I really enjoy the great guests you have on your podcasts. Let me provide some constructive feedback.

1.) You could enhance your podcast by listening to a master interviewer like [name] who really gets the most out of his guest with well prepared and carefully thought out questions.

2.) Given diversified trend trading systems have similar performance it adds value to run many different types of systems with non-correlated returns. Sharing your research on what does not work would be more constructive than your current comments about day trading systems. A great place to start researching other systems is attain and striker which provide hundreds of systems with both backtested and actual track records since go-live. It would be great material for another book to focus on summarizing the 100 most popular trading systems across all strategies with a correlation matrix between them.

3.) It would also be great to have a futures broker as a guest to get their perspective about the pros and cons about having the system executed exactly as specified. If you are aware of another program that has this please pass it along.

4.) Your material is geared toward validating one approach which a good start for the novice. However for those already doing this it would add value to discuss complementary systems/approaches with system developers.

Thanks,

Steven

Thanks for the feedback on interviewee questions. Agreed improvement always possible!

As for other issues:

1. Brokers don’t do much for me. That is for someone else.

2. My recent day trading criticism originated with trend trader Ed Seykota. It was spot on.

3. If my business was all hard core systems types–there would be no business.

As for other complimentary systems what do you mean exactly?

If you ever see that advice, run. Reach for your wallet and run. Fast. The only true measure is the price of the instrument you are trading. An expectation, or prediction, for tomorrow is fool’s gold.