Mike, Can you send me the white paper that was referenced in the Vineer Bhansali podcast? I apologize if this is posted somewhere obvious and I missed it. Normally I’d probably have found it on my own, but having a 3 week old newborn is temporarily draining my productivity! It’d be much appreciated if you could point me in the direction of the research that was discussed. What a refreshing podcast to hear a more mainstream financial institution embrace real trend following.

Thanks,

[Name]

Thanks. Go here for his white paper. And good luck with your new little one!

Also in:

Michael, great show. Do you have additional information about the research/historical performance work done by Vineer Bhansali or is it just the information from the PIMCO pages?

Do you know if this fund actually follows the 100% systematic “simple” trend-follower approach back tested in the article or is this just a bait and switch for a discretionary fund? Do you know the actual rules for the “simple” trend-follower approach back-tested in this paper?

Many Thanks,

[Name]

Best bet is to reach out to them for all questions about their papers.

In many ways, it can all come down to one decision- one choice in one moment that crystallizes a path in front of you. That path is rarely straight and often difficult to navigate, but once that moment has come and gone, the rest- as they say- is history. For Liz Cheval, chairwoman of the close to $150 million managed futures program EMC, that decision was the choice to respond to Richard Dennis’ famed turtle trader ad.

The story of the turtle traders [see my book The Complete TurtleTrader for more] is pretty fantastic in and of itself. Two renowned traders disagree. One says that what they do is unique, while another says that he could train anyone to trade. They make a wager on the issue, an ad is placed in the paper, and the lives of 20 students would never be the same. As the only female selected for the program, Cheval’s life was turned upside down.

After receiving a degree in mathematics from Lawrence University in Appleton, Wisconsin, Ms. Cheval was working as a trade clerk at the Chicago Board of Trade when Mr. Dennis placed his ad in the paper. At the time, women were few and far between in the famed Chicago trading pits. To hear her explain it, it was largely a function of physique.

“When I started on the floor of the CBOT in the early 1980’s… It was difficult for women to compete, given the physical demands of pit trading and the advantages of a larger, heavier frame,” she recalls.

It was on the floor that Cheval found herself drawn to Dennis’ offer. The excitement in the pits over the opportunity was palpable, as resumes were quickly refreshed and rushed to the mail. Cheval found herself being pushed to apply as well, even by those competing against her for a slot (including her employer). When called into an interview, she began to think that maybe she was missing something.

“As I approached the interview, I thought the opportunity with C&D was literally too good to be true,” she explains. “I simply couldn’t believe that a world renowned trader would teach us his methods and give us his private capital to trade. I assumed that there would be a catch, another story revealed at the interview.”

It turned out that the interview was simply the opportunity of the lifetime.

“It was not until the end of the interview, as Mr. Dennis’ top executive explained the nature and the details of the program that I began to believe it was the real deal,” Cheval recounts. “At that point, I became overwhelmed. My throat went dry. My legs were shaking. I could barely walk out of the room. If I understood the true nature of the program at the beginning, I would not have been as collected during the interview and would not have been selected. ”

Being selected may have been the easy part. After the interview began a rigorous amount of training, and the competition was fierce.

“The group was extremely competitive. The dynamic was open, above-board and collegial, but no doubt, everybody wanted to win,” Cheval states.

Even as the only woman in the group, Cheval found herself seamlessly blending into the adrenaline fueled atmosphere. The experience, by and large, was a positive one. She was able to earn the respect of her peers, and believes that working in a group of professional, competitive men helped prime her for professional challenges in the future.

When the training was done, it was time to hit the pavement running. The turtles were hungry to spread their wings and test their mettle. Cheval remembers making phone calls upon completion of the program, trying to gauge the level of interest for outside investors. That former employer who had encouraged her to apply? He became EMC’s first client, investing $1 million.

While it certainly has not been a bed of roses, Cheval has done very well for herself. EMC , which she runs with former turtle Brian Proctor, now has $148.75 million in assets under management, and is as well respected in the industry as you can get, in our opinion. She credits the nuanced strategies involved in managed futures with keeping her in the game. Even with this success, Cheval knows that you need to keep pushing to make it in this industry.

“The ability to adapt to change is the key to long term success in trading. It’s relatively easy to develop a profitable trading strategy over a short time frame. It’s far more challenging to develop a reliable method to continually adapt the strategy to future market conditions,” Cheval states.

Adaptation is especially important in an environment like what is seen today. Managed futures seems to be perpetually under attack by mainstream media pundits and financial advisors, with the bulk of comment being directed toward “greedy speculators.” This misconception, paired with investor frustration over a divergent return stream and increasing government intervention in the markets, can complicate the managed futures conversation, but Cheval is up to the task. In her mind, the theory of the game makes the challenge all the more worthwhile.

Her experience in the industry has granted her a great deal of perspective, and she’s more than willing to share it. The secret to becoming a successful CTA? She’s not keeping mum.

“You need both a successful trading strategy and, more importantly, a reliable method to adapt the strategy to future market conditions. A successful trading strategy requires robust systems and sound risk management principles. The trading strategy is only as good as your research process. You have to identify robust estimators and develop a process to continually adapt the systems based on these reliable estimators,” Cheval says. “You have to be disciplined in executing both trading and research strategies, in good periods and bad. A CTA has to be committed to their strategy whether it is in or out of favor.”

And for all you women out there thinking about entering the field?

“Over the years I encouraged women to manage money because I believed it to be a gender neutral occupation. No one can dispute your contribution based on gender in investment management. Your performance is there in black and white in the P&L report,” states Cheval.

“Go for it. Today the physical advantage of men [in the trading pits] is inconsequential because trading is virtually 100% electronic. I give the same advice to both men and women seeking entry level jobs in managed futures. Technical skills are mandatory. Great thinkers and idea creators need technical applications to test and execute trading strategies. Having those skills is a great way to gain entry or to build your own business.”

However, in our conversations with Cheval, it was her comments on the future of the industry that resonated with us most.

“Money centers will shift, performance will change, but overall, global markets are large and expansive,” she quipped. “Markets and managers will adapt.”

We couldn’t agree more.

Unfortunately, Liz Cheval recently passed away, but her success lives on.

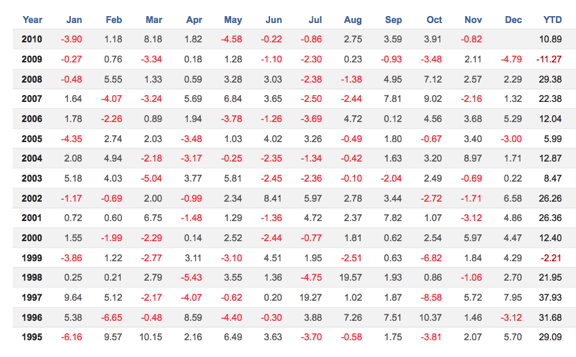

Following a research project that was initiated in 1987, Transtrend B.V. (“Transtrend”) was established in 1991 as an asset manager purely focused on systematic trading strategies. Transtrend’s approach is aimed at exploiting trends in financial and commodities markets and is entirely based on quantitative analysis of typical price behavior in these markets. Transtrend’s trading strategies have no directional bias and can go long or short in their attempt to benefit from price patterns that represent good profit expectancy over time.

Performance (The Enhanced Risk (USD)/Transtrend’s Diversified Trend Program):

Disclaimers:

Our firm can not promise you will earn like returns of traders, charts or examples (real or hypothetical) mentioned. All past performance is not necessarily an indication of future results. Data presented is for educational purposes. This information is not designed to be used as an invitation for investment with any adviser profiled. All data on this site is direct from the CFTC, SEC, Yahoo Finance, Google, IASG and disclosure documents by managers mentioned herein. We assume all data to be accurate, but assume no responsibility for errors, omissions or clerical errors made by sources.

HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.

Robyn Williams: So what’s the risk? Last week we spoke to David Spiegelhalter about Paul the octopus and the maths of probability. This week, what’s behind his actual job, Professor of the Public Understanding of Risk at Cambridge?

David Spiegelhalter: Whatever you think about them, this was a hedge fund that paid for this post in Cambridge. It was a very enlightened move, I think. David Harding who runs it, they make a lot of money and they give quite a lot of it away. And so he supports various mathematical charities in particular and he decided to support this post in Cambridge. One of the nice things is that it pays for my salary, and there is absolutely no guidance or pressure whatsoever to work on any particular topics, and the last thing I do is financial work, I have no idea about financial risk. But I do work in many other areas. I come from a background of medical statistics so I concentrate on medical and health issues. But of course with a job title like this you get pulled into all sorts of stuff, so suddenly you find you have to be an expert on volcanic ash and child safety and you have to be an expert on cycle helmets and things like that. So I am desperately trying to learn up about all these issues all at the same time.

Robyn Williams, CC Wikimedia

Robyn Williams: In general is the public (and I suppose you’re talking about Britain) more leery about risk, about going out, about just being in the world, than it should be?

David Spiegelhalter: That’s a difficult question. One of the things I often get asked by people with a very strict scientific attitude is to say, well, tell me how hopeless people are at dealing with risk, how irrational they are. And I refuse to follow that line of questioning because you just have to think about yourself, about myself; I am not like a rational human being who weighs up everything mathematically, I’m an emotional person who acts largely by their feelings, and that’s how people have dealt with risks since the beginning of time.

The whole mathematics of risk, of probability and ideas like that, are very recent on the scene, they’ve only been around for a few hundred years and we can’t really think that everyone before that was completely stupid and irrational. I think there were probably some quite wise people around who understood, using their feelings, about what uncertainty meant and how to deal with it. We have to deal with uncertainty in our lives all the time.

So saying, I think you could say that there has been in this country (and I’m sure in many other places) far too much of a concentration on trying to say, well, something bad has happened, we’ve got to stop it ever happening again. And this of course is nonsense. Things will always happen, bad things will happen, but there comes a point when actually it’s not worth doing any more because the harms of trying to reduce that risk might easily outweigh the benefits. And the natural area of this of course is in terms of child safety. There comes a point where we must say that we can’t protect our children from everything bad that might happen to them, and sadly this means that on occasions, very rarely, a bad thing will happen to a child.

On the other side of that of course is that if you do try to protect them too much, what other harms are you doing to them in terms of reducing their feeling of adventure, the possibility of learning from failures, of essentially being able to pick themselves up and start again when things go wrong? We can’t protect people and actually it’s not doing them any good to try to protect them too much.

Robyn Williams: Have you crunched the numbers on various aspects of a young child’s life, like walking to school or playing sports where they might get a tonk on the head?

David Spiegelhalter: I haven’t done the sports stuff. One of the difficulties of course is just the data on injuries, for example, it’s ropey because there is no standard way of reporting these things. Sadly of course we can count the bodies because the one thing that is recorded is deaths, and we can look at those statistics. I looked at some recently because of some issues that came up in this country on a father who was being threatened with being reported to social workers because he was allowing his daughter to walk 20 yards to catch a school bus and crossing a road. So here was a seven-year-old girl…it’s extraordinary, seven-year-old children are unbelievably safe, they’ve never been safer. I mean, it’s sad, but something bad will happen to some of them; one in 12,000 seven-year-old girls will die before they’re eight, of all causes. But that means all causes, of illnesses and everything else. If we look at, for example, kids being knocked down, pedestrians, in this country, England and Wales, 50 million people, 1.5 million girls between the age of five and nine, in 2008 one was killed on the roads as a pedestrian. That’s a terrible tragedy, and it was quite a lucky year, and boys have twice the risk of girls, that’s well established…

Robyn Williams: That’s still only two.

David Spiegelhalter: Yes, normally there are a bit more than one, normally it is more than one, it’s just to show that out of 1.5 million, it’s a very small number. So it comes to a point when obviously these are tragedies but things will happen, and surely it’s really important to encourage children to be out and about, to be roaming, to have a life of freedom et cetera.

Robyn Williams: What happened to the father who let his kid go 20 yards to the bus? Was that okay?

David Spiegelhalter: I think the council relented rather. People are fearful, there is a fear of litigation that if something happens somebody is to blame, and schools are very cautious about school trips, and this sets up a very pernicious environment which can just lead to a lack of adventure, lack of risk. The trouble is risk, it’s got bad press, the word ‘risk’ but there are such things as good risks. We take risks. Maybe a better phrase would be that we take ‘chances’, that’s got a better connotation of the fact that taking a chance because something good might happen, we might fail, it might not work, so maybe we should be thinking of risk assessments as chance assessments so we can really think of the fact that when we are uncertain about what might happen, that includes the fact that something good might happen as well as something bad might happen.

Robyn Williams: I suppose one of the terrible things, looking at that, is the sheer cost. You mentioned litigation, of all the former filling-in to see whether someone can get the permission to go out on a school hike or go to places where there might be a cliff-top or, one of the Australian examples, a colleague of mine had to fill in a form which went through five layers of management because there might have been snakes in a suburb of Sydney. I mean, you can get snakes anywhere in Australia but the chances are unbelievably remote, and the snakes are probably hiding. But the cost of litigation and the cost of bureaucracy, has it gone out of control?

David Spiegelhalter: What’s very interesting is that this new government in our country just yesterday has announced that they are going to have a war on unnecessary health and safety bureaucracy, and they’ve got a report that has been written, and they’re hoping to dismantle much of this and to try to stop litigation in these circumstances as well. So things are on the move here, there is a process of change that is going on that’s supported by the government, it’s going to be very interesting to see what happens.

Robyn Williams: So far you’ve mentioned how life is safer than many of us perceive. What about where there are risks that we are rather too blithe about?

David Spiegelhalter: The trouble is the risks we are all so aware of are the horrible things that are going to kill us today, you know, the risk of children being murdered, of car accidents and things like that, yes, we’re really anxious about those. But the bigger risks are often going to be longer term risks and they are not so easy to see. It all sounds rather tedious because people have gone on about it so much, but just our lifestyles, obesity, the way people eat, the lack of exercise, and of course the harm to the environment, the energy security, of what might happen, all these things are much more difficult to put a number on for a start. They are also delayed. We’re talking about things a long time in the future. If we are thinking about climate change of course were talking about things for future generations that we need to be concerned about.

And so you’ve got this difficult balance between what you might call acute risks, things that are going to get us today, and what you might call chronic risks that actually we don’t notice at all at the moment, you know, I can just go around stuffing my face with all sorts of food imported and flown from around the world…I mean, I don’t notice any difference, but I will by the end of my life, there’s a very good chance of that, and my children might notice even more. So this is difficult to do mentally. I know people have trouble with it, I have trouble with it.

Robyn Williams: When the volcano in Iceland (whose name you will immediately tell me) went up, what did you tell the people who were phoning you about the risk to do with flying?

David Spiegelhalter: I try not to say anything at all, and I then got invited onto the government advisory committee on volcanic ash, which was an extraordinary experience, it was very interesting because I’ve just started to get more involved in this disaster committee, which has now carried on to trying to work out the chances of a similar event happening in the future. In the UK now they started a thing called a risk register on which the threats to this country which will require some sort of civil planning are supposed to be recorded, and their rough idea of how bad they are going to be and how likely they are to happen is recorded. That’s quite tricky, you’ve got to work out the chance of another eruption by one of these other Icelandic volcanoes over the next five years and how severe it might be. And we got some data on that.

It’s very interesting analysing data that goes back to about 900 on the intervals between volcanic eruptions, and of course they’re very erratic. We know that predicting volcanic eruptions is unbelievably difficult. So it always has to be a mixture of some statistical analysis where you can say, well, we know roughly what the interval is, that we can state roughly what the probability of it erupting again over the next five years is, but there is inevitably going to be a lot of judgement coming into it as well, and that’s why it has to be teamwork between meteorologists and vulcanologists and statisticians. I think that has proved to me that the business of making these judgements about what the risks are is never just a matter of statistical analysis and mathematics, and you have to bring in scientific judgement, and that means acknowledging scientific uncertainty, the fact that we don’t know what’s going on.

We don’t know what’s going to happen. People are quite happy with being able to…they recognise we can’t say exactly what’s going to happen, but to admit that we don’t even know what’s going on at the moment is quite tricky, and yet that is really what scientists have got to do. They are slightly fearful about it. They look at the climate change debate and they see that, oh my goodness, if we admit we’re not quite sure, we’re going to get pounced on and people will say these scientists don’t know what they’re talking about. I have this naive confidence that if scientists really do actually own up, which they do of course amongst themselves all the time, and if they do that more in public and say, well, we’re not quite sure about everything, it doesn’t mean you shouldn’t act because people act all the time in the face of when they’re not absolutely certain of everything, we’ve always had to do that in our lives. But maybe there are some things we’re not sure about, some things we are sure about.

And I’ve been fortunate enough to be involved with a team in the Royal Society that has written a document on the climate change science which really emphasises the uncertainties and which says, well, we’re pretty sure about this stuff but we’re not so sure about this stuff, and this stuff frankly we haven’t got too much idea about at all. And I feel very happy to be involved in that kind of project where we have an open acknowledgement of where we are. It’s difficult, ignorance is a difficult thing to admit. I think embrace your ignorance, own up, say we don’t know. But then we’ve got to try to find out more.

Robyn Williams: Having looked at the risk of regarding climate change and the uncertainties, how would you assess the reasonableness, the wisdom of doing nothing?

David Spiegelhalter: I’m not a climate scientist so I had to take all my evidence second-hand from what other people have told me, what I’ve read, and discussions I’ve had, and the people I’ve talked to are very clear about the inability to make any precise statements about what’s going to happen. However, the weight of evidence is towards that I’d be very surprised if some pretty severe changes were not going to occur over the next 100 years. And so my feeling is that this is a gamble that I’d rather not take, to be honest, and that we should be doing all we can to try to ameliorate it in any way we can. And just because we’re not totally sure, doesn’t mean we shouldn’t do anything. We act all the time when we’re not totally sure of what’s going to happen.

Robyn Williams: Going to gambling and magic, how do you think people are fooled so easily in that kind of showbiz world?

David Spiegelhalter: I love the cons, we’ve got this guy Derren Brown who does all sorts of illusions, he picks lottery balls, he does all sorts of stuff, and it’s so convincing. He does a lovely trick that we use in classrooms all the time where he stands up and says I’m going to flip a coin ten times in a row and it’s going to come up heads every time. He stands there and he flips a coin and it comes up heads every time and you think, wow, isn’t that cool. Later on in the program he shows how he did it. Of course what he did was stand there for nine hours flipping this coin thousands of times until he finally did ten in a row, and they only show that bit of film.

So this is a really good lesson for the kids, the fact that someone tells you a story and you say, whoa, this is really cool…think ‘what am I not seeing?’ It’s really difficult to think ‘what am I not being told?’ So an example I use is you see a hole-in-one on YouTube, of course you know that they hit this damn golf ball thousands of times before they got a hole-in-one, but they only show that bit of film, and we know that in that situation. But of course we might read on a website about how eating this will cure cancer, or some magical cure; ‘I did this and then I got better’. Well, hang on, what about all the stories of people who did this and they didn’t get better? I want to know all the failures, and we don’t get that information. So this is just one of the many psychological biases we have, it’s just one, it’s a really good one, that we only hear what we hear and it’s really difficult to think about what am I not hearing.

Robyn Williams: David Spiegelhalter is the Professor of the Public Understanding of Risk at Cambridge and, as you heard, was one of those working on the Royal Society’s recent publication on climate.

Darvas places his buy orders for levels that he considers breakout points on the upside. At the same time, he places a stop-loss sell order just below his buy order, so that if the stock does not move straight up after he buys, he will be sold out and his loss cut. “I have no ego in the stock market,” he says. “If I make a mistake I admit it immediately and get out fast.” Darvas thinks his system is the height of conservatism. Says he: “If you could play roulette with the assurance that whenever you bet $100 you could get out for $98 if you lost your bet, wouldn’t you call that good odds?” If he has a big profit in a stock, he puts the stop-loss order just below the level at which a sliding stock should meet support. He bought Universal Controls at 18, sold it at 83 on the way down after it had hit 102. “I never bought a stock at the low or sold one at the high in my life,” says Darvas. “I am satisfied to be along for most of the ride.”

I can’t recall the last time the financial press reported that a 1959 Time Magazine article might actually be good for one’s portfolio health.